You are probably feeling more than a bit overwhelmed and daunted and confused at the immensity of the studying and memorization you think you need to do before the VITA certification test on Wednesday, not to mention working with actual taxpayers in a few short weeks. Yes, you do need to work on practice returns to prepare to develop fluency and comfort in this strange new language, but don't even think that you can accomplish much by mass memorization.

1) It's impossible. The tax code was over 1.4 million words in 2001. Less than a decade later, in 2009, it had more than doubled--to 3.7 million words. And the IRS has supplementary regulations spelling out the manifold operational details that Congress neglected to consider, which increase the total number of words by an order of magnitude.

2) The tax code is a frustrating moving target, because Congress is constantly tinkering with it. Even if you could memorize it, by the time you finished memorizing it, it would have changed.

3) The exam is open book and open note. You will have access to all the same resources during the exam as you will have when working with actual VITA clients (except that you will not be able to ask me questions). But the exams are restricted to very simple in-scope basic tax returns, similar to the first five returns in the Pub 4491w workbook. Most of what you need to know for in-scope VITA returns is handily organized into flow-charts in Pub 4012 and/or in Pub 17. The 1040 Instruction booklet may also be informative. Your paper copies are handy, because you can highlight them and put sticky notes in them, but the electronic copies are also useful because you can use the ^F search function to search for key words.

Go slowly and carefully through the logic of the questions in the flow charts, and you can reason your way through all the questions in the workbook, all the problems on the certification exam, and you will also be able to deal with 95% of the questions that are likely to come up at our VITA site. I may be able to help with a few of the questions you can't handle, and our IRS relationship manager, Joanne Passineau may be able to help use deal with a few more, but others will simply be out of scope for a VITA site and we will need to refer those taxpayers to tax professionals.

The most important thing is for us to know what we don't know--to recognize situations where we need to ask for help or to refer our taxpayers elsewhere. When you see a new wrinkle you've never dealt with before in the practice exercises, don't guess about how to handle it--bring it to my attention.

4) The Intake and Interview Sheet is a key part of our toolkit. Going over all the questions on the sheet with your client is a great way to catch a number of important issues. It is also an IRS requirement for the preparer to make sure that the Intake & Interview sheet is completely filled out for EVERY taxpayer we assist. It will be a course requirement in Eco 391 that you completely go over the intake & Interview sheet and annotate it completely in RED before you open the tax software.

5) Quality Review, teamwork and cross-checking each other are an essential part of our strategy. Remember that nobody is perfect--we are all human and make mistakes (and that includes your professor!) So double-check/triple-check/quadruple-check everything--even if the professor prepared the return, it could be wrong!

It is an IRS requirement that EVERY tax return be quality reviewed by an appropriately certified VITA volunteer (who must be a different person than the original preparer!) We absolutely need two sets of eyes on EVERY return. This job aid for Quality Reviewing is very helpful.

Most importantly of all, we need the taxpayer on our team! Our VITA site has gotten an awesome reputation as the "Go-to" place for taxpayers who want to stay on the right side of the law and play it straight with the IRS, so most of our taxpayers are eager to provide whatever information we need to make sure their return is accurate as possible. (For the small minority who are not, well, it is their prerogative to take their business to more accommodating preparers if they can find them. We will not knowingly prepare a return for a taxpayer who is less than forthright with us in answering our questions. We have so much demand from honest taxpayers that we have no interest in wasting time with anyone who does not want us to prepare an accurate return.)

6) The TaxSlayer software can help (and is essential for e-filing, so our clients can get their refunds promptly), but it's important not to let the software become a "black box," where you type numbers in and get numbers out and don't really understand at all what is going on to transform those inputs into the output.

Spend some time just looking through the 1040 and trying to figure out the lay of the land there, abstracting away from the myriad of details. I know it looks like a mish-mosh patchwork quilt of random odds and ends joined together, a sad artifact due to the fact that Congress has a tendency to cram last minute changes into tax laws many years, with little time to rationalize the forms. Moreover, there is a tendency to constantly add new doodads to the tax code and it's rare that old doodads get subtracted. And yet the 1040 has remained two pages long for decades, even as the tax code has gotten more and more complex. (Yes, there are a growing number of supporting forms and schedules, but ultimately they all have to flow somewhere into the Form 1040.)

The first page of Form 1040 contains just basic but critical demographics and identifying information (name, SSNs, addresses, filing status, and dependents.) Errors here can be disastrous for our taxpayers, so it's really important to get them right.

The second page of Form 1040 (and Schedule 1 if necessary) details the various types of income which taxpayers need to break out separately: wages, interest, dividends, capital gains, self-employment income, unemployment benefits, pension income, etc. You may be wondering why it is broken out this way, instead of all lumped together.

There are a couple reasons why the IRS requires more detail in breaking down income than it used to. One is that part of the increasing complexity of the tax law is that some types of income are treated more generously than other types of income. Very low income people with children are better off if their income comes in the form of wages rather than investment income, due to the refundable Earned Income Credit. Higher income will be taxed more lightly if their income comes in the form of capital gains rather than wages, because such gains are taxed at preferential rates compared to the tax on "ordinary income." Another reason for the more detailed breakdown is that the IRS increasingly uses "document matching" to compare third-party reporting of different income components to what the taxpayer has reported on the return.

The deductions listed on Schedule 1 are so-called Adjustments to Income or "above the line deductions." If you are going to have deductions, above-the-line deductions are as good as it gets for the taxpayer for a couple of reasons: a) they reduce both Adjusted Gross Income (AGI) and taxable income and b) they are useful to everyone, not just itemizers. The below-the-line deductions (highlighted in pink) at the top of page two of the form are not nearly as good a deal, for reasons I will explain.

I'll elaborate here. Obviously, you can see why folks would want to reduce their taxable income--it will generally reduce their taxes. But why should they care about AGI? Well, it turns out that AGI is an important "gateway" to qualifying for many other tax benefits. If your AGI is too high, you may not be able to qualify for certain tax credits or to invest in a deductible IRA, for example, even if your taxable income is quite low. Having too high an AGI can also make your Social Security taxable--again, even if your taxable income is quite low.

It's not really obvious to me why Congress decided that AGI (or its closely allied relative, MAGI, which have been multiplying like Rabbit's friends and relations) should be the gatekeeper of so many tax benefits. It is not as if the type of deductions allowed "above the line" are necessarily any more deserving than those allowed "below the line." (It's worth noting that many taxpayers in our area will have very large below the line deductions this year for casualty losses incurred as a result of the devastating floods which hit very close to our VITA site four months ago. That will reduce their taxable income, but not their AGI. It is not obvious to me why their casualty loss deductions, which are below the line, deserve less weight than somebody else's IRA or student loan interest deduction, which is above the line.)

I digress, but my point is that many things about these colorless lifeless tax forms will come to life when you deal with how they impact the lives of real people, and you will have a new understanding for the trials and tribulations of a tax code with incoherent mixture of good intentions not always well executed, mixed with a random dose of politics and lobbying.

Moving back to our color coded tax return, we have finished with the deduction stage once we subtract our below-the-line deductions and personal and dependent exemptions (speaking of which, any new babies who arrived by midnight Saturday secured a whole year's worth of tax benefits for their parents. This local "first baby of 2012" just missed out. A Buffalo couple had twins born half an hour apart--one will appear on their tax return in 2011, while the other will have to wait until next year.)

So we have now arrived at taxable income. It is time to apply our marginal tax rate schedule to compute the amount of income tax. The chart of marginal rates below comes from Jon Gruber's Public Finance and Public Policy, published a couple years ago, so the breakpoints are slightly different for 2011 returns, due to the automatic indexing for changes in the Consumer Price Index, but the graph below does give you the basic idea of how our tax code works. The current rate schedule is available here, which shows that the key breakpoint for our MFJ taxpayers is $17,000. That is, their first $17,000 of taxable income will be taxed at 10% and any income amounts beyond that will be taxed at 15%. So, for example, a married couple with $20,000 in taxable income would pay 10%*(17000) +15%*(3000) = 1700 +450 = $2,150. The important thing to realize is that once the couple enters a new bracket, only their incremental income over that threshold is subject to tax at the higher rate. Since our VITA site serves taxpayers with gross incomes up to $50,000, we do not expect to see any married taxpayers with federal statutory marginal brackets higher than 15%. It is possible, however, that we will see a few single or MFS taxpayers in the 25% statutory bracket.

But, as they say on late night television, "Wait, there's more!" We have not yet begun to apply credits. Notice that my colored-coded 1040 has a hot pink highlighted section right below the income tax computation. Those represent nonrefundable tax credits. If our hypothetical married couple have a few kids under age 17, or if they paid for daycare in order to work, or if they put in new high efficiency home energy projects, those hot pink nonrefundable credits might wipe their tax bill all the way down to zero. (But not lower than zero--that is why they are called nonrefundable.)

And--again--as they say on late night TV, "Wait, there's even more!" The gold highlighted section at the very end represents the refundable credits. Those can actually knock the taxpayer's liability into negative territory, so that the taxpayer could wind up with refund greater than the amount of withholding.

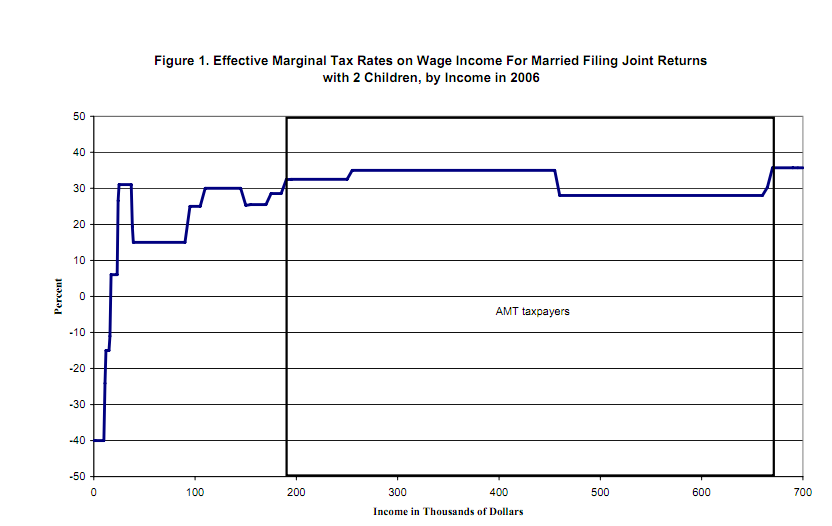

Don't try to absorb it all right now--just immerse yourself in thinking through this incredibly complex world. There's lots to learn and absorb, and we'll also learn that there can be a big difference between the statutory marginal tax rate schedule sketched above and the actual effective marginal tax rate schedule shown below.

But take heart if this all seems like hopelessly confusing gobbledigook at the moment--and come to my helping hours tomorrow so you can work through practice examples which are similar to those on the exam--and to 95% of the situations that come up in practice at our VITA site. You will be prepared before our class begins--with a bang! with the always challenging and bracing VITA certification exam on Wednesday.

No comments:

Post a Comment